Raising in the Worst Market for Emerging Managers

We raised a $5M Fund I in Spring 2023 and a $25M Fund II in Fall 2025. 2023–2025 was the worst three-year fundraising stretch for emerging managers in modern VC history. In 2024, emerging managers captured only 23% of all fund value—a decade low. In 2025, family offices pulled back, endowments came under pressure, and LP capital consolidated to established names.

As LP capital consolidates to tier-1 VCs, VC capital consolidates toward pedigree. The same gravity that pulls LP dollars to Sequoia pulls investment dollars toward pedigreed founders. We know that creates an opportunity.

We invest in anyone, with no bias toward pedigree. We're focused on resilience— founders strengthened by struggle, whether they're Midwest-based, transplants on the coasts, or anywhere in between. A lot of these founders resonate with our thesis and our own non-traditional roots. That shows up in how quickly trust gets built and how those relationships compound over time.

We've been builders too. Our Partners built EquipmentShare—a generational company started in Columbia, MO that went public on the Nasdaq at a $7B market cap. That experience gives us an ethos, perspective, and network that's genuinely different on a cap table. And when the market was pulling capital away from anyone without a coastal brand, we kept investing. Our uniqueness, hustle, values, and resilience resonated with the LP base we targeted.

The Funnel

I spent three months before any outreach refining the story and the materials, getting feedback from Fund I LPs and iterating. The "why" behind Redbud isn't a fundraising strategy—it's the reason we're building a long-standing firm, not just another fund. Our edge is perspective (rural towns, no formal education to a public company), network (Missouri talent and customers), geo (Columbia, MO), and no bias toward pedigree or the hot potato FOMO approach a lot of VCs take. We invest with a long-term lens focused on resilience, which lets us spot outlier talent others gloss over.

We built a prospect list of over 400 names. Met more than 150. Closed over 40%. The reason someone invested or didn’t equally helped us refine our story.

How We Met Our LPs

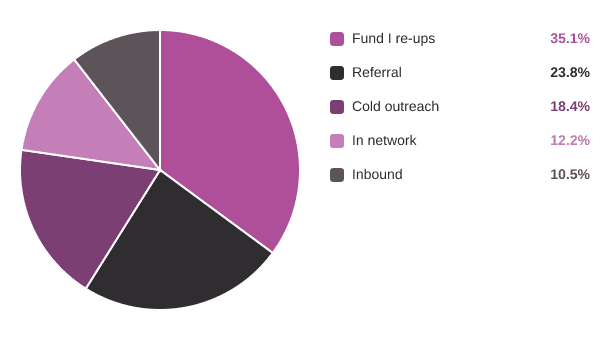

Nearly 60% of the fund came from people who already trusted us or were sent by someone who did. Fund I LPs re-upped at 35% of committed capital and 175% of what they committed in Fund I. Referrals drove another 24%. Cold outreach — fully personalized, no templates — produced 18%, which is high for a market this tight.

CAPITAL SOURCE (% OF COMMITTED CAPITAL)

I refined multiple pitches based on the LP profile. Everyone invests for different reasons — returns, networking, discussing interesting events with friends, supporting locally, diversifying away from real estate, tax-free gains. Every outreach had some uniqueness based on what I thought would resonate. High conversion came from in-person meetings, so I spent a lot of time figuring out the right cold outreach and referral paths just to land the first meeting.

We had less than $10M soft-committed in June 2025 and over $20M by August. The catalyst was having a company pop in June with a 42x mark, putting us in the top 10% across the board in metrics for 2023 fund vintages. We also raised our minimum from $150K to $250K, which resonated with LP prospects and some who had committed to the $150k upped to $250k without us even asking them to do so. A story can only go so far, a strong returns are needed to close real volume.

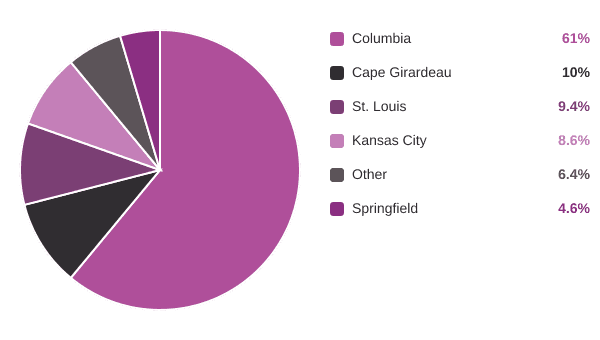

Where Our LPs Are From

61% of capital came from Columbia. We also have strong representation from St. Louis, Kansas City, Cape Girardeau, and Springfield.

LP GEOGRAPHY (% OF COMMITTED CAPITAL)

Trust and values are important in Missouri, and sometimes it takes a while to warm up to someone. We put a lot of time into converting well-known names across the state that could anchor and bring in others. I drove to St. Louis to introduce myself to Jim McKelvey at an event who was a top person on my list to partner with. The first intro was flat, but I found him toward the end of the event and I literally grabbed his arm as he was walking past. I had to scramble to think through an ask so gave him the EquipmentShare going-public pitch and suggested he meet Willy to provide insights as a fellow Missouri founder who has been through the IPO process. We certainly practice what we preach when it comes to being scrappy. It took a few months, but we got him across the finish line. Having a big name like his alongside Sandy Kemper in KC, a previous Boeing CEO, Shelter Insurance, and Mizzou made a real difference in subsequent conversations.

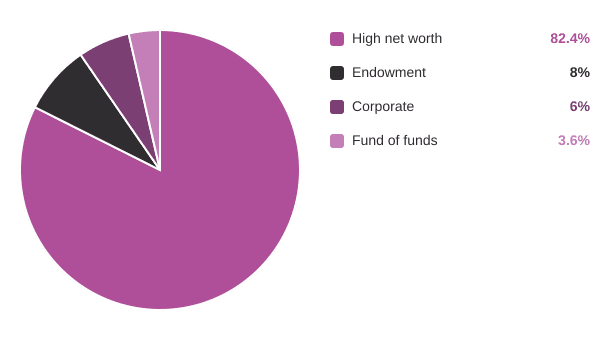

A Relatively Untapped LP Base

Most emerging managers go after the same pool: institutional funds of funds, endowments, and RIAs. We went after operators—people who've built companies in Missouri across steel, construction, manufacturing, payments, healthcare, and technology. 82% of our capital is from high-net-worth individuals. A lot of these folks can be early customers and strategic partners for our portfolio founders, not just check writers. They also resonate with our ethos and mentality with building and investing in companies.

LP TYPE (% OF COMMITTED CAPITAL)

The LP base we built has a ton of alignment with what we're doing. They don't pressure us to play the hot potato game, i.e., chasing quick markups on flashy deals. That lets us be disciplined and patient, investing with a long-term lens on durable companies.

One way to frame the investment to an LP: think of it like a high-risk 401(k) targeting ~30% annualized returns, tax-free via QSBS, with a 10+ year lockup. It's not for everyone. For the right person, someone who's built a business, understands and appreciates risk, and has minimal allocation to tangential asset classes, it’s a great opportunity to diversify a portfolio.

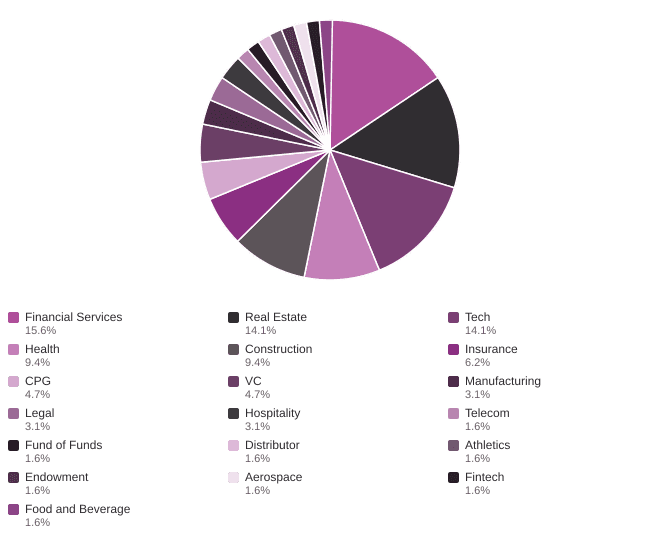

INDUSTRIES OUR LPS COME FROM (% OF LP COUNT)

Why LPs Work With Us

LPs invest for different reasons and we lean into that. There is a lot of psychology that goes into fundraising and it’s critical to understand why that person chose to meet with you. We pitch differently depending on who we're sitting across from:

Returns | Think of it like a high-risk 401(k) targeting ~30% annualized returns, tax-free via QSBS, with a 10+ year lockup. Not for everyone. But, for the right person, nothing else looks like it. |

Network | LPs get access to the same room as founders who've taken companies from zero to nine figures. |

Vanity | Being in a VC fund is more interesting than a CD. LPs get early access to what's being built before it's mainstream. |

Diversification | Most of our LPs are heavy in real estate or public equities. Early-stage venture is an uncorrelated bet. |

Altruism | A lot of our LPs are Missouri operators who genuinely want to see the ecosystem grow. We're the vehicle for that. |

Alignment | We don't have LPs who pressure us toward quick markups or flashy deals. We can invest in durable businesses regardless of whether they're the hot thing right now. |

Notable LP and Advisor Companies

Our LP base is largely composed of over 50 operators who've built companies in Missouri across many industries. A lot of these folks can be early customers and even strategic investors for our portfolio founders.

EquipmentShare Construction Tech 7,000+ employees Founders Took public on the Nasdaq at a $7B market cap. | C2FO Fintech ~600 employees Founder KC-based working capital marketplace used by Fortune 500s globally. Raised $568M. | Boeing Aerospace 170,000+ employees Previous CEO Fortune 100 with deep aerospace and enterprise operator expertise. | Meta Technology 79,000+ employees Early engineer, still at the company Deep technical and product perspective on the cap table. |

Square / Block Fintech ~6,000 employees Founder. Works with over 4 million businesses worldwide. | Zapier Tech / SaaS ~740 employees Founder Columbia, MO roots. YC top 25, $5B valuation — one of the most capital-efficient SaaS companies ever built. | Trinity Products Steel Manufacturing Private Founder Missouri-based manufacturer with deep industrial operator reach across the state. | SGC Food Service Food & Beverage Private CEO Regional distribution leader and early customer resource for portfolio founders. |

Upgrade Fintech / Hospitality ~1,500 employees Executive Fast-growing digital lending platform with multi-billion dollar valuation. | Shelter Insurance Insurance ~1,100 employees Corporate LP Columbia-based insurer — one of Missouri's most recognized institutions. | Veterans United Fintech / Lending 4,300+ employees Founder Columbia-based, one of the largest mortgage lenders in the US. | AMCA Aerospace Manufacturing Private Founder Portfolio of manufacturers backed by Founders Fund. |

What Matters

Getting the right names in early: Trust travels through relationships. I focused on converting a handful of meaningful names first: Jim McKelvey, Kemper, Shelter Insurance, and Mizzou. Once those were in, the next conversation started from a different place. It takes time and a lot of nos to get there, but each one compounds. The deck got updated after each pitch. There was always something to learn from every yes or no.

Getting people in the room: My Partner, Willy, and I started hosting dinners and happy hours. Short pitch, good people, low pressure. Attendees brought friends. Some of those friends committed without ever coming to an event. They just saw that someone they trusted was in. In-person conversion was consistently higher than anything else we did, so a big part of the job was just figuring out the right path to get the first meeting.

Treating it like a sales process: I set a goal of $20M with one close by October. We closed $24.5M. I kept tight communication with every soft commit and moved on quickly from anyone who was on the fence. A maybe in the pipeline is worse than a no. It blocks your time and pulls focus from people who are genuinely in. Every outreach was personalized. When I pitched, I rarely opened the deck. The best conversations didn't need it.

Adjusting the framing for each LP type: We talked to 400+ prospects and had 150+ meetings. Real estate investors were the hardest. Framing it as a high-risk 401(k) targeting 30% annualized tax-free returns with a 10+ year lockup landed much better than talking about DPI or IRR. Operator LPs got a different conversation than community-motivated ones. Figuring out which type you were sitting across from, and adapting fast, made a big difference.

Last Thoughts

If we'd raised in 2021, we'd probably have a different fund. Easier markets attract tourists in LPs and in founders. The tighter market forced us to be sharper about who we raised from, more creative about how we reached them, and more honest about what we were building.

We invest in people strengthened by struggle. It's been a grind over the last five years from the Scale Accelerator, to a $5M Fund I in 2023, to a $25M Fund II in 2025, to taking EquipmentShare public on the Nasdaq. At Redbud, we demonstrate the same thing we look for in founders.

Cheers to building in places you call home. 🥂