Amazon went public in 1997, three years after it was founded. eBay took three years, Yahoo! took two, and Google took six. The IPO frenzy during the Dot-Com boom was the result of a perfect combination of hype, incentives, and access. On August 16, 1996, E*Trade debuted on the NASDAQ, entering the public markets at 14 years old. The platform gave retail investors easy access to public markets, pumping more trade volume into the internet vertical. The internet was a once in a generation innovation that the market was more than happy to pay for, further incentivizing founders to IPO. The founders wanted easy access to capital, and IPOs gave them access to that capital. IPOs also allowed VCs to exit their positions, and let the average American invest in the hottest new internet companies. The music began to fade, however, on March 13, 2000, when news of Japan entering a global recession triggered a selloff across all internet stocks, bursting the Dot-Com bubble. Unlike the early 2000s, the driving forces of the market today are the private companies.

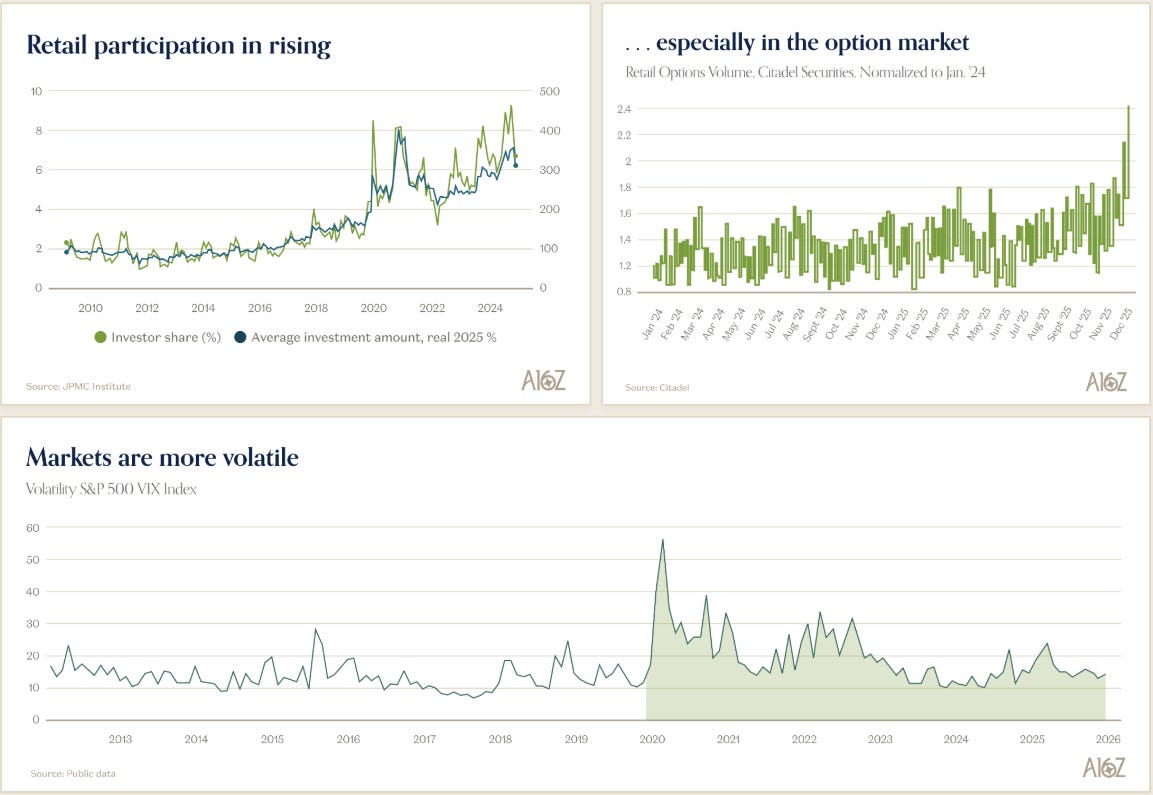

During the Dot-Com boom, access to a wide base of retail investors gave founders access to sufficient amounts of capital. But, private equity AUM over the last decade has risen to $12 trillion and is expected to double to $25 trillion over the next decade1. The influx of capital to the private markets has allowed startups to stay private for longer and facilitate more value creation in private markets. You can also point to rising interest rates as another factor keeping companies stashed away in the private markets. Rising rates mean a higher discount rate baked into financial models, which disproportionately affects startups whose value largely stems from future cash flows, as opposed to profitable companies with large cash flows in the near-term. Since 2021, the majority of billion-dollar deals have shifted to the private side. Increased volatility has also chipped away at the attractiveness of public markets. Below are charts from a16z’s State of the Markets slide deck that help visualize the increase in post-COVID volatility.

While access to private capital, rising interest rates, and increased volatility have kept more startups in the private domain, private markets lack one structural feature that public markets have: price discovery. Public markets exist to discover the true price of an asset, whereas private markets are built on agreed upon prices. Every VC knows that the companies who raised in 2021 aren’t worth what they were valued at in 2021. Although this is an extreme example, many later-stage rounds are valued based on forward revenue multiples and expectations of future exponential growth. It can take a company many years for the private valuation to match the scrutiny of public markets. Despite this, you can find companies that refuse to raise a down round in order to hold on to their lofty valuations. Even the wildly successful companies had to deal with the consequences of 2021 valuations. Superstar startup, Brex, valued its 2021 Series D at $12.1B. When it was announced in January that they were being acquired for $5.2B by Capital One, late-stage investors lost money, as some lacked liquidation preferences.

Private markets have an extremely important purpose in the startup ecosystem. They sidestep the short-termism and expensive capital imposed by the public markets, giving startups the freedom to scale with less investor punishment. However, when capital is too cheap and valuations are too lofty, those benefits become a liability. In some cases, companies overhire, creating a poor cost structure that the short-termism of public markets would scrutinize. And this lack of scrutiny creates unresolved pricing mismatches that complicate exits, undercutting the benefits of cheap capital. It should also be noted that a mix of FOMO, misaligned incentives, and the need for massive funds to deploy swaths of capital, competing for a few good opportunities, all contribute to higher and higher private market prices. The result is VC hot potato where deals are pushed around until someone is stuck with the consequences of diverging from scrutinized prices.

Although you could argue that one just shouldn’t play hot potato with valuations, one bad actor forces the hand of all investors. The biggest risk to VC and growth investing isn’t losing money, but missing out on the winners. Those familiar with the power law know that success compounds on success, resulting in exponentially large returns from the true winners. The economics of early-stage and growth investing necessitate adherence to the power law, such that not having one true winner undermines the potential to return a fund and raise more capital. Because the power law dictates this stage of investing, going for the winners is non-negotiable. This creates the cycle of FOMO and private market price inflation. The cycle only stops if someone steps back. Either VCs stop handing out cheap capital, founders stop accepting it, or LPs stop investing in funds that promise artificial returns.

To continue this train of thought, if you undermine the economics of growth investing, at what point does the current ecosystem break? You could argue that the result is that the majority of growth investors will post mediocre performances with the occasional winner. But why wouldn’t institutional investors just throw their money into the biggest names? If capital allocators conclude that smaller players with less sway to win top deals aren’t worth investing in, then would that result in the consolidation or the slow death of the growth middle market? Certainly, either outcome would shift the balance of power within the venture ecosystem.

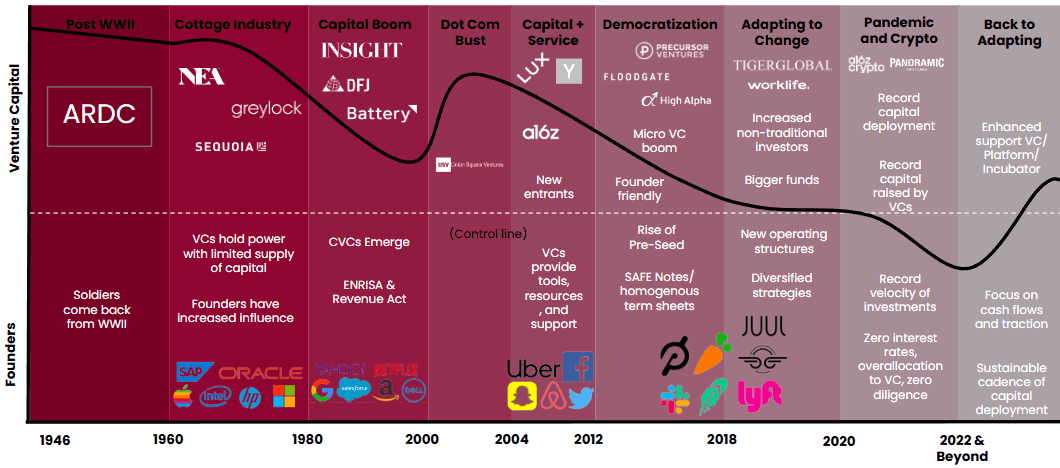

I’ve included a graph, representing the balance of power between investors and founders over time. However, it should be noted that influence now lies in the hands of founders, given the graph cuts off in 2022.

Stripe announced a tender offer at $159 billion in late February, providing liquidity to employees. This round represented a 49% increase in valuation, surpassing the high watermark set in 2021. This is being interpreted as Stripe delaying their IPO, as the market remains weak. The small appetite for IPOs has led major players to seek liquidity via new avenues. Robinhood launched Venture Fund I, giving retail investors the ability to purchase stakes in top-performing startups at NAV, without the price scrutiny of public markets. However, several critics have pointed out that the introduction of retail investors via this fund seems like a plea for liquidity amongst a weak IPO market. Other institutional funds like Fidelity, also offer access to private markets, but Robinhood’s approach offers daily liquidity and high concentration. Reluctance to IPO is a departure from the late 1990s eagerness to IPO, but still represents an underlying issue. By targeting secondary markets and retail investors, investors are trying to salvage their 2021 vintages by avoiding punishing public markets for private markets that are more willing to purchase at favorable prices.

While startups and investors may prefer the private markets, continued step-ups in valuations over the extreme 2021 prices make soft-landings increasingly difficult. Brex couldn’t manage to save their late-stage investors, Stripe is continuing its run in the private markets, and Robinhood introduced broader retail participation in public-averse private companies.

Public markets should gain more consideration as a means of soft-landing rather than just a risky haircut to high valuations. Investors need to exit their positions, and while M&A offers more certainty around price, valuation downgrades through M&A unevenly assign losses to the hot potato losers. While secondary rounds provide liquidity, those prices aren’t being held accountable by the opinion of the public market, resulting in a prolonged departure from large scale, clean distributions. But IPOs keep late-stage investors in the game allowing them to recover losses through public market price appreciation. As the gap between public and private pricing persists, the resulting question is whether late-stage investors can continue absorbing the full weight of price corrections. Public market volatility is real, but delaying IPOs only widens exposure because each new private round exposes capital to prices that have not been vetted by public markets. If winners continue to shy away, distributions will continue to fall and too many late-stage investors will be forced to absorb uneven losses, threatening the slow death of the growth middle market.

Startups are Staying Private Longer (CNBC)

More $1 Billion+ Deals in Private Markets

Stripe Secondary Sale Valuation